A number of papers (on agricultural productivity, conflict, food security, and impacts of climate change, for example) use cropland cover data as controls. How good are these data?

Here’s the abstract of a paper (open access) from Wei and co-authors:

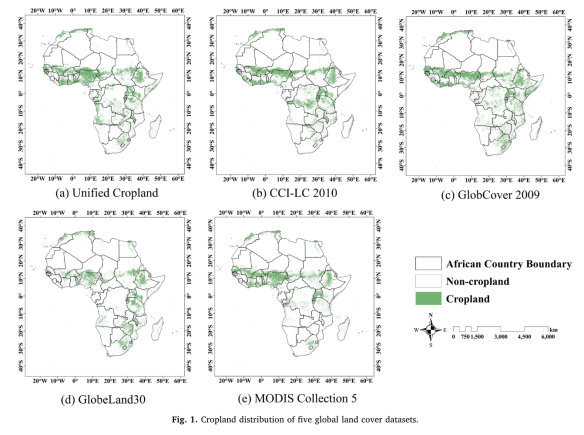

Accurate geo-information of cropland is critical for food security strategy development and grain production management, especially in Africa continent where most countries are food-insecure. Over the past decades, a series of African cropland maps have been derived from remotely-sensed data, existing comparison studies have shown that inconsistencies with statistics and discrepancies among these products are considerable. Yet, there is a knowledge gap about the factors that influence their consistency. The aim of this study is thus to estimate the consistency of five widely-used cropland datasets (MODIS Collection 5, GlobCover 2009, GlobeLand30, CCI-LC2010, and Unified Cropland Layer) in Africa, and to explore the effects of several limiting factors (landscape fragmentation, climate and agricultural management) on spatial consistency.

The results show that total crop-land area for Africa derived from GlobeLand30 has the best fitness with FAO statistics, followed by MODISCollection 5. GlobCover 2009, CCI-LC 2010, and Unified Cropland Layer have poor performances as indicated by larger deviations from statistics. In terms of spatial consistency, disagreement is about 37.9 % at continental scale, and the disparate proportion even exceeds 50 % in approximately 1/3 of the countries at national scale.We further found that there is a strong and significant correlation between spatial agreement and cropland fragmentation, suggesting that regions with higher landscape fragmentation generally have larger disparities. It is also noticed that places with better consistency are mainly distributed in regions with favorable natural environments and sufficient agricultural management such as well-developed irrigated technology. Proportions of complete agreement are thus located in favorable climate zones including Hot-summer Mediterranean climate(Csa), Subtropical highland climate (Cwb), and Temperate Mediterranean climate (Csb). The level of complete agreement keeps rising as the proportion of irrigated cropland increases. Spatial agreement among these datasets has the most significant relationship with cropland fragmentation, and a relatively small association with irrigation area, followed by climate conditions. These results can provide some insights into understanding how different factors influence the consistency of cropland datasets, and making an appropriate selection when using these datasets in different regions. We suggest that future cropland mapping activities should put more effort in those regions with significant disagreement in Sub-Saharan Africa.

Here’s what they did:

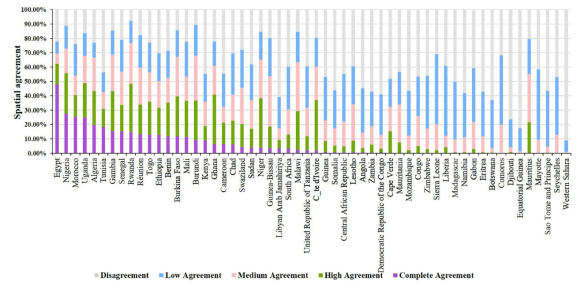

…. we compared the spatial agreement of cropland to assess the consistency of five datasets in the same location. These datasets were overlapped to generate a new composite map revealing whether and where the original datasets agreed on the same locations (Yang et al., 2017). Pixels of the composite map were assigned values ranging from 0 to 5. The highest value 5 represents the complete agreement, where all five datasets were consistent in cropland identification for a pixel. As the value decreases, spatial consistency between these crop-land datasets decreases. The lowest value with value 1 means that only one dataset identifies the pixel as cropland.

The best consistency of five datasets occurs in Egypt, with the complete agreement value of 47.86 %, while the highest disagreement is in Western Sahara, whose spatial disagreement is 91.08 %.

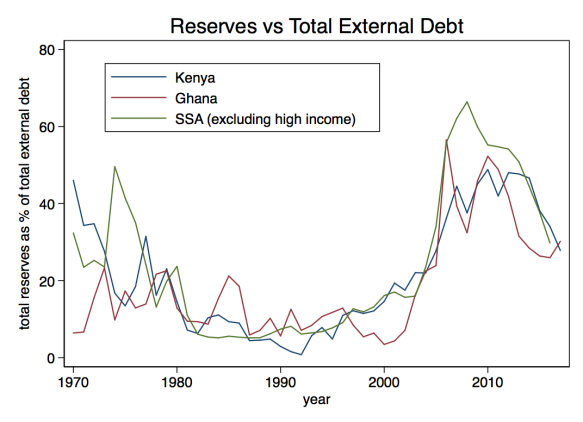

Countries in sub-Saharan Africa accumulated external debt at a faster pace than low- and middle- income countries in other regions in 2017: the combined external debt stock rose 15.5 percent from the previous year to $535 billion. Much of this increase was driven by a sharp rise in borrowing by two of the region’s largest economies, Nigeria and South Africa, where the external debt stock rose 29 percent and 21 percent respectively.

Countries in sub-Saharan Africa accumulated external debt at a faster pace than low- and middle- income countries in other regions in 2017: the combined external debt stock rose 15.5 percent from the previous year to $535 billion. Much of this increase was driven by a sharp rise in borrowing by two of the region’s largest economies, Nigeria and South Africa, where the external debt stock rose 29 percent and 21 percent respectively.

The oil price shock is adversely impacting the economy. Angola’s oil basket is projected to average US$53 per bbl in 2015, from slightly over US$100 per bbl in 2014, leading to large declines in fiscal revenue and exports. While oil production has recovered following the completion of maintenance work, non-oil GDP growth is expected to decelerate to 2.1 percent in 2015. The industrial, construction and services sectors are adjusting to the decline in private consumption and public investment and lingering difficulties to obtain foreign currency. Inflation is projected to reach close to 14 percent by end-2015, exceeding the National Bank of Angola (BNA)’s 7-9 percent objective. The 2015 budget will allow the central government deficit to fall to 3.5 percent of GDP, compared to 6.4 percent last year. Public debt, however, is projected to increase significantly to 57.4 percent of GDP, of which 14.7 percent of GDP corresponds to the state-owned oil company Sonangol, by end-2015. The external current account deficit is expected to reach 7.6 percent of GDP in 2015; and international reserves to drop to US$22.3 billion (about 7 months of 2016 imports) by end-2015. Meanwhile, a wide spread emerged between the parallel and primary market exchange rates, pointing to an imbalance in the foreign exchange market.

The oil price shock is adversely impacting the economy. Angola’s oil basket is projected to average US$53 per bbl in 2015, from slightly over US$100 per bbl in 2014, leading to large declines in fiscal revenue and exports. While oil production has recovered following the completion of maintenance work, non-oil GDP growth is expected to decelerate to 2.1 percent in 2015. The industrial, construction and services sectors are adjusting to the decline in private consumption and public investment and lingering difficulties to obtain foreign currency. Inflation is projected to reach close to 14 percent by end-2015, exceeding the National Bank of Angola (BNA)’s 7-9 percent objective. The 2015 budget will allow the central government deficit to fall to 3.5 percent of GDP, compared to 6.4 percent last year. Public debt, however, is projected to increase significantly to 57.4 percent of GDP, of which 14.7 percent of GDP corresponds to the state-owned oil company Sonangol, by end-2015. The external current account deficit is expected to reach 7.6 percent of GDP in 2015; and international reserves to drop to US$22.3 billion (about 7 months of 2016 imports) by end-2015. Meanwhile, a wide spread emerged between the parallel and primary market exchange rates, pointing to an imbalance in the foreign exchange market.