I am currently working on a project on commodities in SSA and have been amazed both by the region’s mineral wealth and how much of it gets stolen by local elites in cahoots with large MNCs. It is one thing to read about corruption from 30,000 feet. Getting an up-close view is another matter. The examples of the two Congos are instructive…

Congo-Brazzaville is one of the top oil producers in Africa. It is also a dirt poor country, with over 70% of its people living below the poverty line. Like in Equatorial Guinea (and other petro-states in the region), the ruling cabal in Brazzaville has turned the country’s oil wealth into private property – the symbol of which is the president’s son’s extravagant expenditures in European capitals (For more details see below).

[youtube.com/watch?v=VpGU1hsuSpU&feature=player_embedded]

These details of the sleaze around oil revenues in Congo were unearthed, by among others, Elliot Associates, a “vulture fund.”

Across the river in the other Congo (Congo-Kinshasa aka DRC) another vulture fund is trying to get Kinshasa to pay up. The vulture fund, FG Hemisphere, paid $3.3m for the debt to a Bosnian state-owned company, and then went ahead and sued for $100m in the courts of Jersey to recover the debt. Recently the Privy Council in the UK, the final appeals court, ruled in favor of Kinshasa. For more on this see the Guardian (here, here and here), which has been following this particularly case closely.

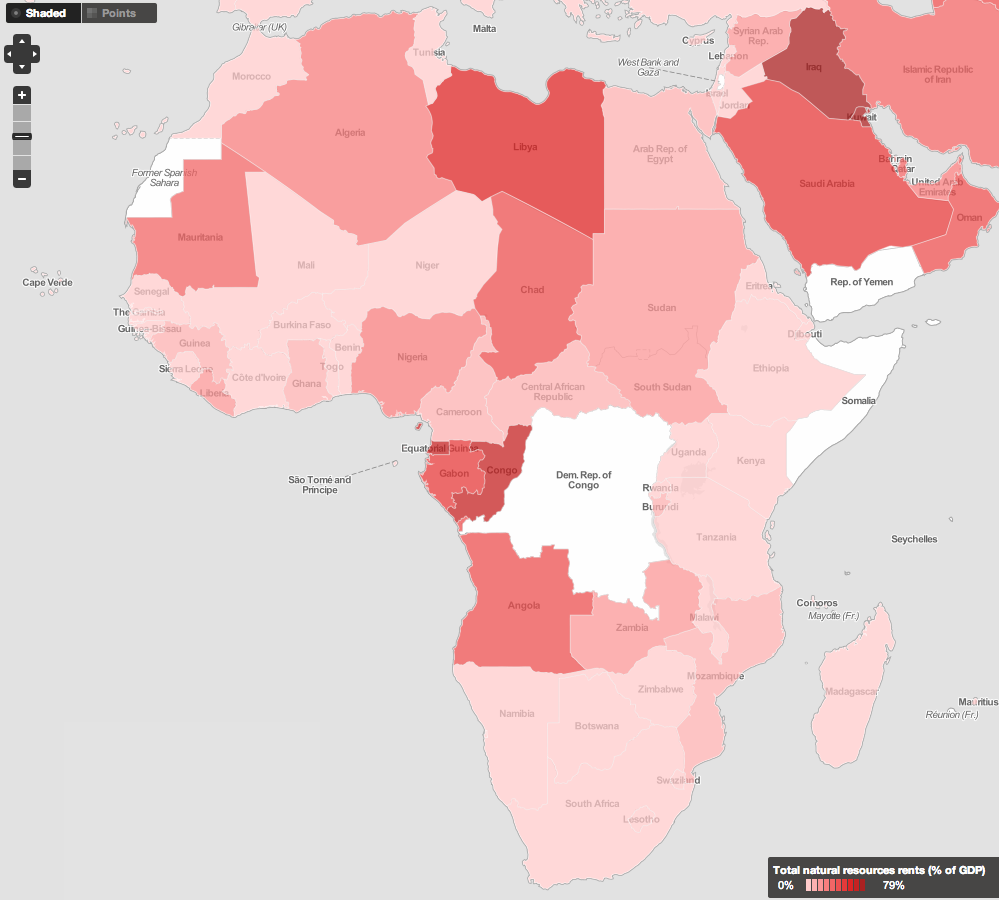

The Democratic Republic of Congo has a mineral wealth estimated to be around $24 trillion. It is also one of the least and poorest governed places on the planet. A recent report indicated that as much as 5 billion dollars in revenue from minerals has disappeared from the state coffers in the recent past.

Should Brazzaville and Kinshasa be forced to pay up?

Opinion over the utility of venture funds is divided. There are those that blame them for going after the poorest countries, asking for taxpayers to pay for their rulers’ (sometimes dead and gone, like Mobutu) largesse. But there area also those who contend that the best way of making rulers less willing to steal is by forcing them to pay up their debts – especially considering that debt forgiveness alone cannot end corruption.

Eric Joyce, writing in the Guardian puts it thus:

Campaigners have always maintained that if FGH is unable to collect the debt then the money will go instead to public works in the DRC. This is simply not true. The doctrine of “sovereign immunity” applies across the world and it is therefore not possible for any creditor, “vulture” or otherwise, to access funds that have a sovereign purpose – that is, public expenditure. Creditors can only target cash being used to trade.

With this in mind, perhaps the do-gooders campaigning for debt cancellation and recovery of stolen monies could team up with vulture funds. The latter have both the expertise and financial incentive to go after monies hidden in foreign bank accounts and shell companies registered in tax havens. Just a thought.