Africa Confidential has a great piece analyzing leaked documents from PwC, the professional services firm, showing the various arrangements that enable multinational companies to evade taxes in Africa. You can read the whole piece here (gated).

- One of the measures PwC advised multinationals to take was to create a wholly-owned Luxembourg-based subsidiary which would hold the rights to intellectual property used by the rest of the group. The rest of the group would then pay licensing fees to the Luxembourg-based subsidiary which, by agreement with the authorities, would be granted tax relief of up to 80%……

- A second tax avoidance mechanism simply involved the companies becoming incorporated in Luxembourg. In 2010, Luxembourg concluded an agreement with several companies of the Socfin (Société financière) agribusiness group, which was founded during the reign of Belgian King Leopold II by the late Belgian businessman Adrien Hallet. The companies chose Luxembourg as their base and made an agreement under which their dividends were subject to a modest 15% withholding tax, a lower figure than those in force where their farms are located (20% in Congo-K and Indonesia, 18% in Côte d’Ivoire).

The art of hiding profits

Altogether, Socfin subsidiaries in Africa [in Sierra Leone, Nigeria, Liberia, Cote d’Ivoire, and Cameroon] and Indonesia produced 123,660t. of rubber and 380,770t. of palm oil in 2012. The combined turnover of its main African subsidiaries reached €271 mn. in 2013. The list also includes the 100%-owned Plantations Socfinaf Ghana Ltd. (PSG) and Socfin-Brabanta (Congo-Kinshasa). Socfin also holds 88% of Agripalma in São Tomé e Príncipe and 5% of Red Lands Roses (Kenya).

- A third mechanism involves cross-border lending within a group of companies. Companies registered in Luxembourg are exempt from tax on income from interest.

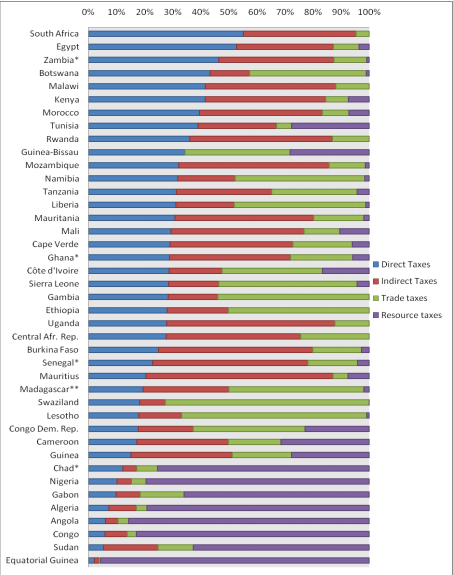

According to the Thabo Mbeki High Level Panel report between 1980 and 2009 between 1.2tr and 1.4tr left Africa in illicit flows. These figures are most likely an understatement. Multinationals, like the ones highlighted by Africa Confidential, accounted for 60% of these flows.

Alex Cobhan, of the Tax Justice Network, has a neat summary of the various components of illicit financial flows (IFFs) and how to measure them. He also proposes measures that could help limit IFFs, including: (i) eliminating anonymous ownership of companies, trusts, and foundations; (ii) ensuring that all bilateral trade and investment flows occur between jurisdictions which exchange tax information on an automatic basis; and (iii) making all multinational corporations publish data about their economic activity and taxation on a country-by-country basis.

Alex Cobham blogs here.