This is from EY’s 2018 Africa Attractiveness report:

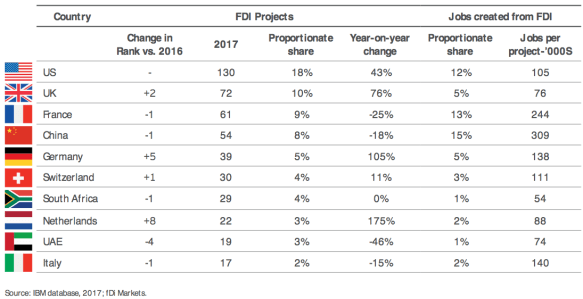

Mature market investors continue building on their deep-seated ties to Africa. In 2017, the US remained the largest investor in the continent, with a noticeable 43% growth in FDI projects. Western Europe, another well-established investor, also built on its already strong investments into Africa, up by 17%. However, emerging-market investments fell, with both intra-regional and Asia-Pacific investment declining by 12% and 13%, respectively. This is, in part, attributable to slower emerging markets growth and weak commodity prices.

It is odd that this report does not give the dollar values of FDI projects. But it has a summary of the distribution of projects and the number of jobs created. This is an important indicator because it reveals projects’ real impact on the real economy — as opposed to projects designed to create enclave economies. Notice that China is far and away the leader on this metric — with Chinese projects resulting in nearly three times as many jobs as American projects (FDI from Italy appears to be particularly good at producing actual jobs).

Here’s another interesting observation on the sectoral focus on FDI projects from the report:

Over the past decade, we have discussed a shift from extractive to “consumer-facing” sectors, thanks to Africa’s growing consumer market. Mining and metals, along with coal, oil and gas, previously the major beneficiaries of FDI flows, have slowed, while consumer products and retail (CPR), financial services, and technology, media and telecommunications (TMT) have risen.

In 2017, FDI shifted somewhat, with consumer-facing sector investments slowing, in line with challenging operating conditions. The focus changed instead to manufacturing, infrastructure and power generation.

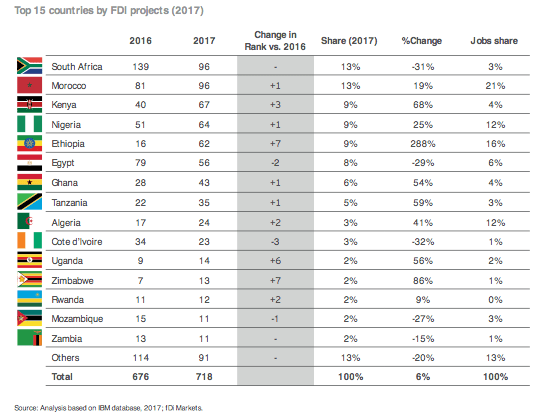

And finally, here are of “FDI-to-jobs” conversation rates. On this measure South Africa and Kenya stand out for their apparent inefficiency in converting FDI projects into jobs.