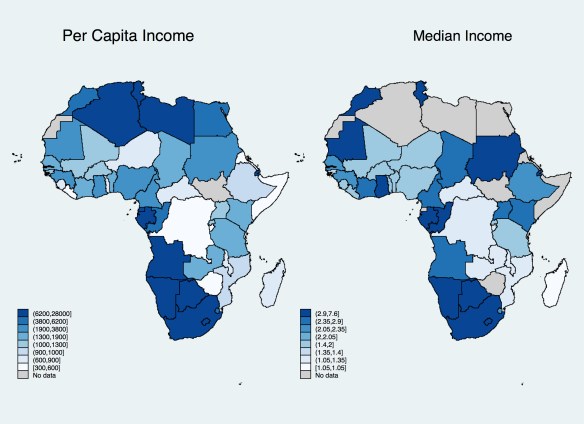

CGD’s Anna Diofasi and Nancy Birdsall compiled median income (2011 PPP) data for 144 countries. In the data they find interesting cases of a mismatch between median and per capita incomes:

the median reflects how much the person at the 50th percentile of the income distribution earns (or spends), giving us a better picture of the well-being of a “typical” individual in a given country. Take Nigeria and Tanzania: in 2010, Nigeria’s GDP per capita (at PPP) was $5,123; Tanzania’s stood at only $2,111. This suggests that Nigerians were more than twice as well off as Tanzanians. Yet, if we compare consumption medians, a different picture emerges: a Nigerian at the middle of the income distribution lived on $1.80 a day, while his or her Tanzanian counterpart had 20 cents more to spend, at $2 a day.

I got curious and made maps of median (2011 $$) and per capita (2010 $$) incomes on the Continent.

What is going on with median incomes in Central Africa from CAR through to Mozambique? Also, what’s up with Zambia?

Over the past decade, lower tariffs within the East African Community (EAC) have boosted regional trade, offering the five member countries a route to faster growth. According to the IMF’s latest projections, growth in the EAC region is expected to reach 5.9 percent in 2011—a noticeably faster growth rate than in the rest of sub-Saharan Africa.

During 2000–10, intraregional exports between Burundi, Kenya, Rwanda, Tanzania, and Uganda tripled—from nearly $700 million to nearly $2 billion. Rwanda’s exports have grown the most during this period, from about $1.6 million to $156 million, but are still a fraction of those of the region’s largest economy, Kenya. Kenya’s exports to the other EAC members were about $1.2 billion in 2010. In contrast, export growth in Burundi—the poorest member—has remained constant and imports have declined, mainly because of civil war and inferior infrastructure, such as airports, roads, and docks, which is needed for trade.

At the same time, EAC countries have been exploiting new markets, including those within the region. Exports to other EAC countries are now as high as exports to the euro area, followed by exports to the rest of Africa and developing Asia.

Moreover, tariffs for EAC members in general have fallen substantially. Over the past 15 years, tariffs in the EAC region have been cut from an average of 26.1 percent in 1994 to an estimated 9.2 percent in 2011. But some members are reluctant to completely scrap tariffs because of the loss of tax revenue.

Given the substantial reduction in tariffs and the sizable increases in exports within the EAC, the region is set to achieve sustained higher growth. But to achieve middle-income status over the next 10 to 15 years—a goal of most countries in the region—the EAC must address a number of issues, such as strengthening of institutional reforms and reduction of nontariff barriers. Removing these remaining obstacles could facilitate faster growth and greater diversification of the region’s exports.

Members of the East African Community

The EAC was established in 2000 by Kenya, Tanzania, and Uganda, with Burundi and Rwanda joining in 2007. Its objectives are promotion of duty-free trade and free movement of capital and labor among its members. Despite a slow start, a common market for the region was established in July 2010.

Regional markets

In addition to promoting local sources of economic growth, Africa is moving rapidly to foster regional integration aimed at creating larger continental markets. The most inspiring of such efforts is the June 2011 launch of negotiations for a Grand Free Trade Area (GFTA) stretching from Libya and Egypt to South Africa.

The proposed GFTA would merge three existing blocs, including the Southern African Development Community, the East African Community (EAC), and the Common Market for Eastern and Southern Africa.

Proponents envision that GFTA will include 26 countries with a combined GDP of over $1 trillion and an estimated consumer base of 700 million people. This significant market will appeal to foreign as well as domestic investors. Local industrial and agricultural development will take center stage, but many inputs will come from abroad, and talks on developing this tripartite free trade area are already under way.

Larger trading blocs facilitate the economic growth that in turn enhances the expansion of the middle class. It is estimated that the free trade area initiatives of the three existing regional blocs in Africa led exports among the 26 member states to increase from $7 billion in 2000 to over $32 billion in 2011.

These efforts build on ongoing integration efforts in the EAC, including a customs union, common market, common currency, and political federation. The five member countries (Burundi, Kenya, Rwanda, Tanzania, Uganda) count 135 million people with a total GDP (at current market prices) of about $80 billion, representing a powerful consumer base.

The region is currently negotiating the establishment of a monetary union to advance and maintain sound monetary and fiscal policy and financial stability. The negotiations are attempting to take into account the limitations of the euro area by including provisions for fiscal integration and financial stabilization. If adopted as envisaged, the monetary union would yield Africa’s first genuine regional economy, which would attract foreign direct investment and bolster consumer spending and growth of the middle class.

LikeLike